Burgundy’s €300m vineyard sale marks a new frontier for collectible wine estates

Burgundy’s top vineyards move from scarcity premium to institutional asset, after a €300m Côte d’Or sale resets price expectations

For years, Burgundy’s Côte d’Or has operated according to its own financial gravity. Prices that would look extravagant in almost any other agricultural market have become familiar here, where tiny parcels, historic names and global demand for collectible wines compress enormous value into a few rows of vines. Yet even by Burgundy’s standards, the 2025 vineyard land market has crossed a psychological threshold.

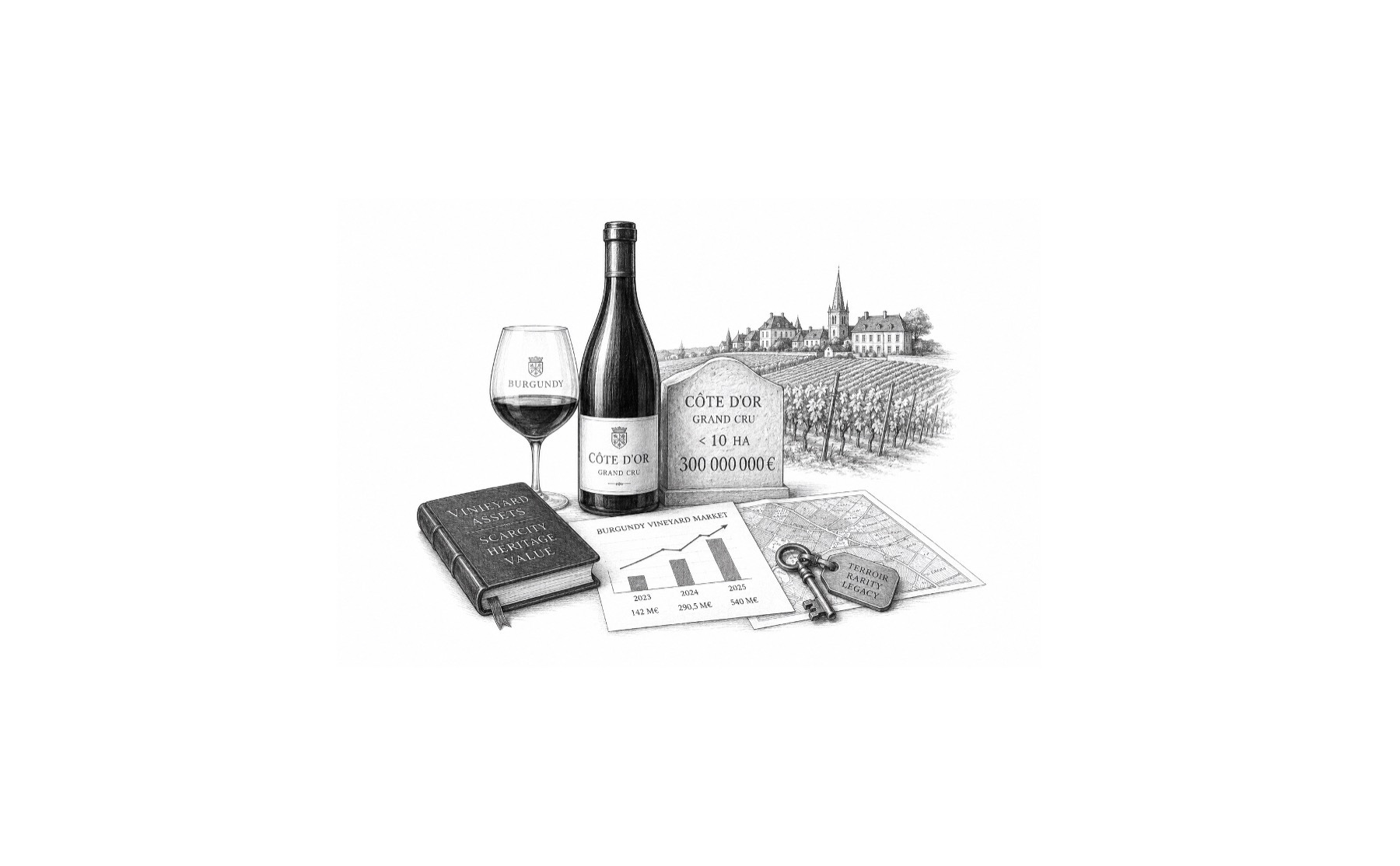

According to SAFER Bourgogne-Franche-Comté, one transaction in the Côte d’Or exceeded €300m for less than 10 hectares of vines. On a simple hectare basis, that implies a level around €30m per hectare. A second transaction reached €50m. For Philippe de Segonzac, director of SAFER BFC, the significance lies not only in the price, but in the form of the market in which it occurred. Transactions above €100m or €200m have previously been seen in company-share deals, where the underlying assets can include vineyards, buildings, stocks, brands and shareholder accounts. But on the physical land market itself, SAFER says such financial volumes are unprecedented.

That distinction matters. Company-share transactions can obscure the value attributed specifically to vineyard land. A direct physical vineyard sale is a cleaner signal. It tells the market that certain Côte d’Or assets are no longer merely expensive vineyards. They are trophy holdings, strategic wine assets and, increasingly, investment-grade scarcity objects.

The Burgundy vineyard market has long been bifurcated, but 2025 has made the divide more visible. At national level, the average sale price for AOP vineyard land fell 3% over the year to €171,400 per hectare. In the wider Bourgogne-Beaujolais-Savoie-Jura region, however, the average rose 4% to €307,500 per hectare. Even that regional figure understates the reality of elite Côte d’Or and Yonne parcels. As de Segonzac warned, a single deal can tilt the market. In Burgundy, averages are often less informative than outliers.

The scale of the outlier is startling. SAFER estimates that the one exceptional €300m transaction represented 56% of the total value of the regional vineyard market in 2025, excluding company-share exchanges. The region recorded 709 vineyard transactions, up 11%, covering 680 hectares, up 27%, for a total value of €540m, up 82%. The market had already doubled the previous year, rising from €142m in 2023 to €290.5m in 2024. In 2025, it did not merely grow again; it entered another category.

The reported buyer behind some of the Côte d’Or acquisitions is FICOFI, associated with Deepak Rao, with interests cited in names such as Bâtard-Montrachet, Bonnes-Mares and Échezeaux. These are not ordinary appellation holdings. They sit in the symbolic and commercial core of collectible Burgundy, where land is rarely available, bottles are globally allocated, and a vineyard’s name can carry as much financial power as an address in Mayfair, Manhattan or the 8th arrondissement.

For collectors, such prices confirm what the secondary market has suggested for years: Burgundy’s top crus are no longer priced solely on agricultural yield or even on wine production economics. They are priced on rarity, succession, brand adjacency and permanence. The land cannot be replicated. The appellations cannot be expanded at will. The names have been built over centuries. In a world where elite wine increasingly behaves like a portable store of cultural and financial value, owning the source has become the ultimate position.

That does not mean the whole of Burgundy is experiencing the same phenomenon. SAFER is careful to stress that viticultural land remains a highly specific and limited-volume segment. It does not reflect the broader agricultural land market of the region. But it does lift the image and economic momentum of the sector. In Burgundy, prestige at the top radiates downward, supporting confidence even as other French wine regions face much harsher conditions.

This contrast with Bordeaux is especially revealing. While Bordeaux has been wrestling with oversupply, weakening demand in certain categories and vineyard devaluation, Burgundy remains comparatively resilient. Bernard Lacour, president of SAFER BFC, describes Burgundy as better able, for now, to withstand the wider wine crisis seen elsewhere. His explanation lies in segmentation. Burgundy’s offer is fragmented by appellation, village, climat, producer and parcel. Demand is equally segmented. Collectors, merchants, importers and investors are not buying “Burgundy” in the abstract; they are hunting for precise names, precise slopes and precise signatures.

That structure creates a powerful price mechanism. When supply is tiny and demand is global, a handful of transactions can reprice expectations. A famous Côte d’Or parcel may not trade for decades. When it does, the buyer is not simply acquiring vines; they are acquiring future allocation power, historical continuity and a position in one of the world’s most supply-constrained luxury ecosystems.

This is why the physical market matters. It is the foundation beneath every other Burgundy market: bottle allocations, estate valuations, négociant strategies, inheritance negotiations and investor positioning. When land values move so dramatically, the implications flow outward. Families reassess succession. Estates consider partnerships. Investors look for minority entries or holding structures. Young growers face an even higher barrier to entry. Merchants and private clients recalibrate what secure access to top fruit might be worth.

The most delicate question is generational renewal. Burgundy’s romantic image rests on family estates, human-scale domaines and growers tied intimately to their parcels. Yet when a few hectares can command hundreds of millions of euros, preserving that model becomes harder. SAFER says it is still supporting installations across Jura, Saône-et-Loire, Côte-d’Or, Yonne and Nièvre, including progressive acquisition of small parcels in prestigious AOCs. But the arithmetic is unforgiving. The more the top end of the market financialises, the more succession becomes both a family question and a capital question.

For Lacour, the objective is to preserve farms of human scale, with strong involvement from those who actually run them. That is more than nostalgia. It is also a defence of Burgundy’s competitive identity. The region’s global prestige depends not only on famous land but on the credibility of those who work it. If the vineyard becomes too detached from the grower, Burgundy risks weakening the very model that made its land so valuable.

Still, the market’s immediate message is clear. Burgundy is not immune to the pressures affecting wine consumption, production costs and climate risk. There are areas of caution, including parts of Beaujolais depending on crus and routes to market. Investors are thinking harder before committing capital. But SAFER sees no broad or surprising zones of severe weakness across the regional vineyard market. Burgundy and Jura, in its reading, continue to hold up well.

The result is a market of extremes. On one side are French wine regions where vineyard land can struggle to find buyers. On the other are Côte d’Or crus where a single sale can dominate an entire regional year. The gap between land that no longer attracts successors and land that global capital is willing to chase has rarely been wider.

For intelligence readers tracking France’s collectible wine estates, the €300m sale is therefore not just a headline number. It is a signal of structural scarcity meeting concentrated capital. It shows that the most coveted Burgundy vineyards are being valued less like agricultural land and more like irreplaceable cultural infrastructure. They produce wine, but they also produce status, access, memory and market power.

The next phase will test the region’s ability to absorb this wealth without losing its balance. Burgundy’s historic strength is that it has always converted smallness into value. Its danger is that the same smallness now attracts capital at a scale that may distort ownership, succession and access. The 2025 figures suggest that the Côte d’Or has entered a new financial era. The open question is whether Burgundy can keep its human-scale soul while its most collectible vineyards trade at prices that belong to the world of trophy assets.