Bonnes-Mares Grand Cru

Burgundy’s powerful grand cru of dual identity, where Chambolle finesse meets Morey authority and collectibility depends on producer.

Overview and Historical Context

Bonnes-Mares sits at the apex of Burgundy’s hierarchy as a red Grand Cru of the Côte de Nuits, spanning the communes of Chambolle-Musigny and Morey-Saint-Denis. Official Bourgogne Wines data puts the appellation at 14.99 hectares, with a five-year average annual production of 484 hectolitres, or roughly 64,372 bottles, making it materially larger than Musigny yet still very small by any normal global fine-wine standard. Its collector importance rests on a distinctive combination: it is historically canonical, stylistically singular, and sufficiently scarce to matter, but not so tiny that every bottle trades like a trophy. For investors, that means Bonnes-Mares is not best understood as one monolithic “asset”; it is a producer-filtered market in which the climat is elite, but the real pricing power and liquidity are concentrated in the top domaines.

The documented historical record is unusually strong. The current INAO cahier des charges notes that the climat was already ranked in “première classe” by André Jullien in 1816 and in “première cuvée” by Dr. Lavalle in 1855, confirming that Bonnes-Mares was already perceived as first-rank territory long before modern branding and global speculation altered Burgundy’s market structure. The same INAO text says the AOC was recognized by decree in 1937, while the official Bourgogne Wines appellation sheet gives 8 December 1936 as the creation date. The safest reading is that Bonnes-Mares belongs to the original 1936–1937 founding generation of Burgundy’s AOC system, with minor date variation depending on whether one cites the initial recognition or the decree framework.

Its prestige is also cultural rather than merely commercial. Bourgogne Wines states that the vineyard has been known by this name since the late Middle Ages, though the etymology remains uncertain, and the wider Climats of Burgundy—of which Bonnes-Mares is part—were inscribed on the UNESCO World Heritage List on 4 July 2015. That UNESCO recognition does not change legal status or bottle price on its own, but it reinforces the standing of Burgundian climats as precisely delimited, historically continuous sites whose identity is tied to the exact parcel, grape, and know-how. For collectors, this matters because Bonnes-Mares is not a generic grand cru label; it is one of the reference climats through which Burgundy’s terroir-based value system is understood.

Among critics, collectors, and producers, Bonnes-Mares has long occupied a fascinating middle position. It is not typically spoken of with the ethereal reverence reserved for Musigny, nor with the monopole mystique of Clos de Tart, but it is often prized precisely because it marries stature with a more assertive, broad-shouldered personality. Official Bourgogne Wines describes it as rich, fleshy, mouth-filling, clearly structured, and at times “a little wild,” while noting the long-running debate over the Chambolle and Morey expressions within the cru. That tension between perfume and power is central to its prestige and to its investment profile: Bonnes-Mares attracts both purist Burgundy collectors and buyers who want a grand cru with greater authority and more obvious early scale than many Chambolle wines offer.

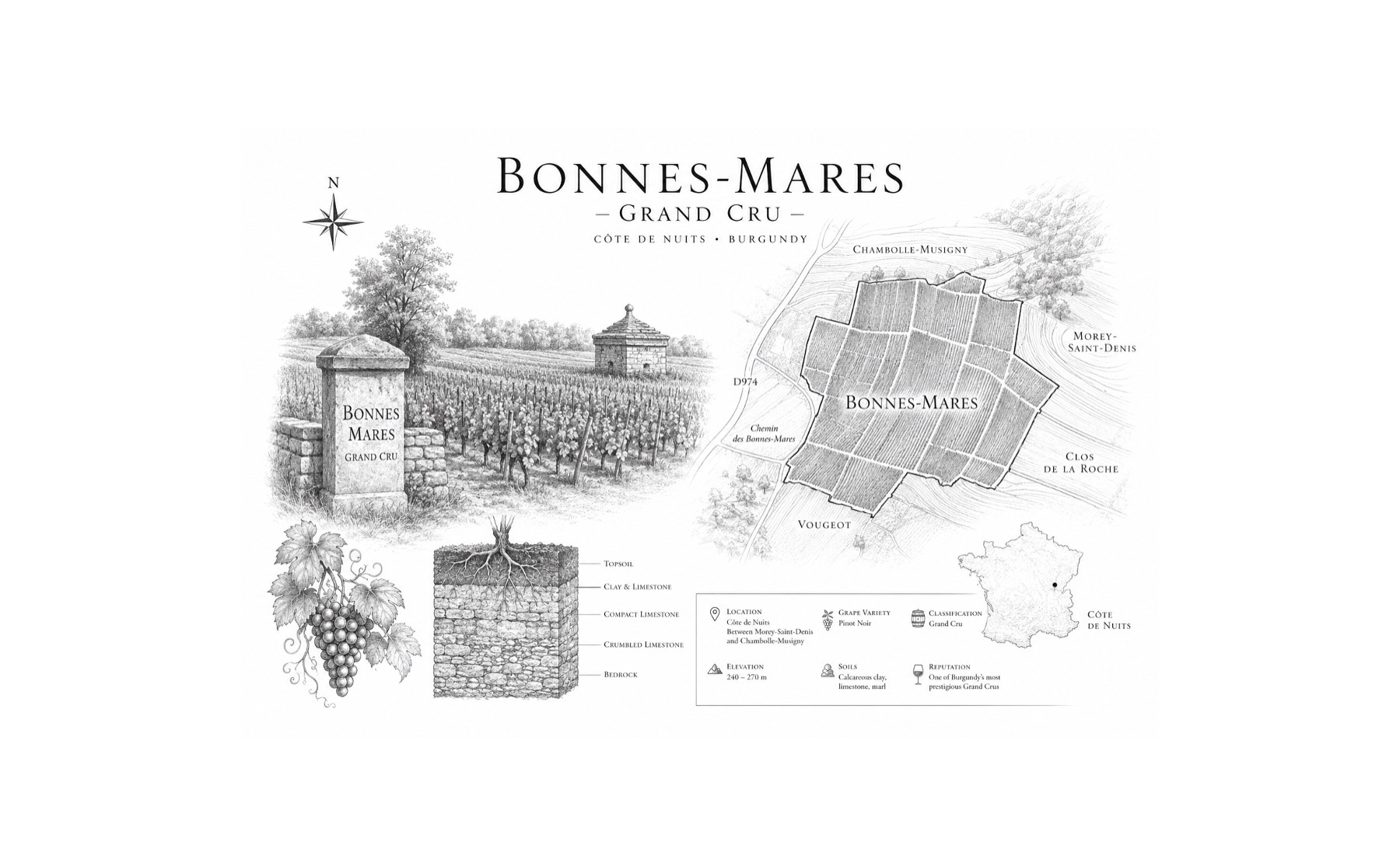

Terroir and Viticulture

What makes Bonnes-Mares distinctive is that its identity is not merely geographical but geological. Official Bourgogne Wines places the climat just south of Clos de Tart, on an easterly exposition at roughly 250 to 280 meters in altitude. The site is gently sloped, with limestone pavement and white marl beneath clay-flint soils around 40 centimeters deep; the surface soils are described as light, gravelly, and brown to reddish in color. The current INAO cahier des charges adds an important viticultural explanation: a marly band crossing the vineyard, together with argillaceous topsoils rich in iron oxides, creates moderate fertility and a notably balanced water regime that can evacuate excess water while still preserving parsimonious moisture in dry periods. This is exactly the kind of hydraulic balance that serious Pinot Noir sites need if they are to ripen fully without losing structural definition.

Producer-level technical sheets sharpen that picture. Roumier’s official Bonnes-Mares sheet explains the cru as a fusion of “Terres Blanches” and “Terres Rouges”: the upper part consists of calcareous marls rich in Ostrea acuminata fossils, while the lower part is clay-limestone over compact Bathonian rock of the Premeaux type. Dujac’s technical sheet describes the same east-facing climat with reddish-brown soil in the eastern part containing crinoidal limestone fragments and lighter, oyster-shell-rich marl soils toward the west. In practical terms, Bonnes-Mares is one of the clearest examples in Burgundy of a cru whose personality is built from the interaction of two soil families rather than a single homogeneous profile. That helps explain why the best wines can seem at once floral and stern, sensual and architectural.

The official planting rules are strict even by Burgundy standards. The INAO rules specify Pinot Noir as the principal grape, while Chardonnay, Pinot Blanc, and Pinot Gris are permitted only as accessory varieties in mixed plantings, limited in total to 15% within each parcel. Minimum planting density is 9,000 vines per hectare, the minimum natural alcohol is 11.5%, and the target yield is 42 hl/ha with a ceiling yield of 49 hl/ha. In reality, benchmark producers usually work below the legal cap. Roumier’s current technical sheet gives 30 hl/ha for its Bonnes-Mares, and Jasper Morris’s note on Bruno Clair’s 2022 cites 35 hl/ha as an “ideal yield.” For collectors, that distinction matters: legal yield is a regulatory framework, but realized yield at the top estates is often much lower and more quality-driven.

Ownership is highly fragmented, and fragmentation is one of the cru’s central scarcity drivers. The largest and most market-visible holders include Comte Georges de Vogüé at about 2.7 hectares, Bruno Clair at 1.6413 hectares, Georges Roumier at 1.3919 hectares, Domaine Dujac at 58 ares, and Jacques-Frédéric Mugnier at only 36 ares. Mugnier’s own site states that its annual production varies between just 900 and 1,500 bottles. That range alone illustrates why Bonnes-Mares cannot be analyzed as though it were a single commodity. A collector buying Mugnier is buying a micro-production luxury object; a collector buying Bruno Clair is entering a more available but still rare grand cru market; a collector buying de Vogüé or Roumier is stepping into a blue-chip Burgundy arena with deeper secondary-market recognition.

On viticulture, the appellation shows a meaningful but not neatly quantifiable movement toward organic, biodynamic, and lower-intervention practice among leading estates. Dujac’s official estate page says the domaine was certified organic in 2011 after beginning trials in 2001 and extending organic farming across the whole estate by 2008. Becky Wasserman’s current estate sheets describe Mugnier’s Bonnes-Mares as sustainably farmed and Bruno Clair’s as worked with sustainable, organic-oriented practices. Arlaud’s market presence is explicitly tied to biodynamics. At the regional level, the BIVB says Bourgogne is rolling out the WinePilot carbon-footprint tool and targeting carbon neutrality by 2035 through a 60% reduction in CO2 emissions plus compensation for the balance. For Bonnes-Mares, the relevant takeaway is not that every grower farms the same way; it is that the leading reference producers increasingly frame quality, site expression, and long-term resilience together.

Wine Style and Aging Potential

The official style of Bonnes-Mares is unusually coherent across sources. Bourgogne Wines describes the wines as rich, fleshy, mouth-filling, with a clearly defined structure, delicately tannic power, and aromas evoking violet, humus, and underbrush; it also states that the wines can age 30 to 50 years. Mugnier’s description emphasizes frankness, solidity, earthy character, red fruit, mineral nuance, and occasional undergrowth tones. Roumier’s technical sheet goes further, attributing red and black-fruit richness to the red soils and spice, white flowers, and peony-like notes to the white soils, with the final blend bringing together fruit, minerality, richness, and firmness. In shorthand, Bonnes-Mares remains one of Burgundy’s most convincingly “complete” grand crus: it rarely offers the sheer aristocratic silk of Musigny, but the best examples often compensate with depth, grip, and a more tactile sense of expansion on the palate.

Young Bonnes-Mares is typically broad-shouldered, dark-fruited, and structurally obvious. Even at the most refined estates, it tends to show more muscle than the average Chambolle-Musigny grand or premier cru. The top recent reviews underline that pattern. William Kelley wrote in Robert Parker’s Wine Advocate in January 2024 that Roumier’s 2022 Bonnes-Mares was “deep and resonant,” “layered and concentrated,” and dense without turning hulking, scoring it 96–98 points; for the 2023, available via a current retail citation, Wine Advocate’s note gives 98 points and describes a cool, layered, impeccably balanced wine with sweet, powdery tannins. On de Vogüé’s 2022, Millésima lists 95 from Wine Advocate, 94 from Allen Meadows, 98 from James Suckling, and 90 from Neal Martin, a spread that captures both the wine’s stature and the fact that Bonnes-Mares can divide tasters when power outruns immediate charm.

With bottle age, the cru tends to move less toward fragility than toward integration. The official Bourgogne Wines sheet speaks of a power common to both the Chambolle and Morey sectors, softened over time into a more nuanced whole. That is consistent with the best mature examples, which often develop forest floor, game, black tea, rose, truffle, and sous-bois characteristics while retaining a core of savory intensity. The important cellar point is that Bonnes-Mares often needs more patience than buyers expect from Chambolle. Mugnier explicitly recommends aging its wine for at least five to ten years; Bruno Clair says ten years minimum; de Vogüé’s market material places its Bonnes-Mares in a ten- to thirty-year window; and Roumier’s technical sheet gives an average guard time of five to twenty years, which likely underestimates what elite vintages can achieve under ideal provenance.

Vintage sensitivity is real, and Bonnes-Mares expresses it clearly. Official BIVB vintage summaries describe 2022 as “generous and promising,” 2021 as exceptionally low in volume and offering delicate wines to enjoy young, 2020 as a “remarkable” or “great classic” vintage, 2019 as a year in which the “magic of years ending with a nine” ultimately worked, and 2015 as “simply sublime.” Jancis Robinson’s Burgundy red vintage chart aligns well with that framing: 2022 is good to excellent and suitable for medium- to long-term drinking; 2021 is light, elegant, and earlier-drinking; 2020 is richly fruited and built for long aging; 2019 is reliably good to excellent with concentration; 2015 invites comparisons with 2005; and 2005 itself is described as exceptionally good. For collectors, that makes Bonnes-Mares a cru where great years should still be bought for the long term, but more delicate years can be strategically useful because the appellation’s natural structure often preserves seriousness even when the season does not deliver monumental density.

Top Producers and Benchmark Wines

At the blue-chip end, Georges Roumier remains the reference name for Bonnes-Mares as both collectible and market object. Roumier farms 1.3919 hectares, equally divided between the two major soil types according to its own 2023 technical sheet, and vinifies the sections separately before blending for elevage and bottling. The official regime is highly classical—manual harvest, 65% destemming, indigenous yeasts, no fining or filtration, 16 months in older oak with 30% new barrels—yet the market treats the wine as one of Burgundy’s most sought-after red grands crus. Current public data show a 2021 iDealwine estimate of €926 per bottle, a 2022 retailer listing of €1,395, and a 2019 retail listing of €1,695. Critically, the wine continues to score at the top end: Wine Advocate gave the 2022 96–98 points in January 2024, and the 2023 is shown at 98 points in a current retail citation. For both collectors and investors, Roumier Bonnes-Mares functions as a genuine benchmark.

Comte Georges de Vogüé is the other essential blue-chip name, though with a different profile. Market material and importer documentation place the estate’s Bonnes-Mares holding at roughly 2.7 hectares, making it one of the largest proprietors in the cru. Millésima notes that most of de Vogüé’s holding lies on the red-clay terres rouges, which helps explain the wine’s reputation for darker fruit, more concentration, and a firmer, more muscular temperament than the domaine’s Chambolle wines. For the 2022, Millésima lists scores of 95 from Wine Advocate, 94 from Allen Meadows, 98 from James Suckling, and 90 from Neal Martin, with a current retail price of €777 per bottle. iDealwine’s current estimate for the 2019 is €501, suggesting that while de Vogüé’s Bonnes-Mares is unquestionably grand cru and highly collectible, it typically trades at a discount to the very top Roumier tier. For buyers, that often makes it one of the most intellectually attractive entries into upper-echelon Bonnes-Mares.

Jacques-Frédéric Mugnier occupies a more connoisseur-driven niche: tiny production, very high prestige, and a style many collectors consider among the most graceful interpretations of the cru. Mugnier’s official site states that the domaine has only 36 ares planted in 1961, 1980, and 1988, and produces between 900 and 1,500 bottles annually. Becky Wasserman’s estate sheet describes a fully destemmed vinification, ambient fermentation and maceration in open wooden vats, 18 months in barrel with only 15% new oak, followed by time in stainless steel before bottling. Critically, Millésima lists the 2020 at 94–96 from Wine Advocate, 95 from Allen Meadows, and 17.5 from Jancis Robinson, at $1,750 per bottle; iDealwine’s estimate for the 2019 is €903. That combination of minute production and critical standing makes Mugnier one of the most desirable Bonnes-Mares for private cellars, though its market is somewhat narrower and more specialist than Roumier’s.

Domaine Dujac is the key name for collectors who want Bonnes-Mares with a more overt whole-cluster and aromatic-signature identity. The domaine’s official technical sheet gives a holding of 58.01 ares on an east-facing slope between 278 and 296 meters, with soils ranging from reddish crinoidal limestone ground to lighter marl with oyster shells. Dujac’s official estate page states that the domaine has been certified organic since 2011. Public market references show a 2019 iDealwine estimate of €639 and a current 2023 in-bond listing around €905.33 ex-VAT per bottle. On the critical side, William Kelley scored the 2022 Bonnes-Mares 95–97 in Wine Advocate in January 2024. Dujac’s Bonnes-Mares is therefore highly relevant for both drinking and collecting, though the secondary-market premium remains more measured than Roumier’s or Mugnier’s.

Below that top quartet, Bruno Clair and Arlaud are especially important because they demonstrate that Bonnes-Mares remains a serious collector’s cru even below the blue-chip ceiling. Bruno Clair’s official sheet documents 1.6413 hectares, southeast exposure, vines dating to 1946, 1962, 1978, and 1980, 30–50% whole bunches, and about 45% new oak; Jasper Morris scored the 2022 at 96–98, while iDealwine currently estimates the 2021 at €315. Arlaud’s 2019 is estimated by iDealwine at €313, and current retail material for the 2022 calls out biodynamics and a 94–96 Burghound score. In practical terms, these wines sit in the collector zone rather than the pure trophy zone: appreciable scarcity, genuine aging capacity, and strong terroir expression, but with less universal auction depth than the most famous labels.

One important caveat belongs here. Public information on the rarest Bonnes-Mares bottlings—especially Domaine d’Auvenay and some Leroy-linked cuvées—is far thinner and less consistently transparent in accessible sources than for Roumier, de Vogüé, Mugnier, or Dujac. For an authoritative appellation profile, it is better to acknowledge that limitation than to overstate certainty. At appellation level, the market is best read through the producers for which parcel, score, or pricing evidence is robust and repeatable.

Classification, Production, and Scarcity

Bonnes-Mares is officially a Grand Cru appellation of the Côte de Nuits, and on labels the words “Grand Cru” must appear immediately below the appellation name in lettering of the same size. The cru is red-only in practice and in the official Bourgogne Wines presentation, with Pinot Noir as the legal core variety. Its current vineyard size is 14.99 hectares, and the five-year average production cited by Bourgogne Wines is 484 hl or 64,372 bottles. By Burgundy standards, this is scarce but not vanishingly scarce; that is part of what makes the cru interesting. There is enough wine for multiple producer identities to exist, yet far too little for demand to broaden without causing price strain in the top tiers.

Comparative scarcity clarifies Bonnes-Mares’s place in the hierarchy. Official Bourgogne Wines data show Musigny red at 10.13 hectares and roughly 33,915 bottles on a five-year average, Clos de Tart at 7.39 hectares and about 26,334 bottles, and Clos de la Roche at 16.73 hectares and roughly 71,421 bottles. Bonnes-Mares therefore sits between the smallest icons and the somewhat broader large grands crus: materially scarcer than Clos de la Roche in total volume, but much less scarce than Musigny or Clos de Tart. That helps explain market behavior. Bonnes-Mares can achieve extremely high prices when the producer is iconic, but the climat’s aggregate scale prevents it from becoming uniformly stratospheric across the board.

Scarcity also operates at the producer level, where the picture becomes much tighter. Mugnier’s 900 to 1,500 bottles per year are archetypal micro-luxury Burgundy. Dujac’s 58 ares and Roumier’s 1.3919 hectares are not publicly translated by the estates into bottle counts in the sources reviewed, but the surface areas alone indicate small-volume grand cru production. Laurent Roumier’s Bonnes-Mares is described by iDealwine as about 600 bottles from a 0.14-hectare parcel. In other words, even within a grand cru producing around 64,000 bottles in aggregate, several of the bottlings that actually matter to collectors are produced in quantities better measured in hundreds or low thousands.

Availability is correspondingly sharp. Auction and retail records repeatedly emphasize original cases, magnums, and tightly held allocations. Christie’s 2017 direct-from-the-cellars sale of Domaine Comte Georges de Vogüé highlighted numbered front labels and personalized back labels for bottles and magnums taken directly from the domaine’s cellars, which is exactly the sort of provenance enhancement serious buyers seek. More recent Christie’s lot pages for de Vogüé’s 2022 Bonnes-Mares specifically note three-bottle and magnum lots in original wooden case. Scarcity in Bonnes-Mares, then, is not just about how many bottles exist; it is also about how many appear with impeccable provenance and collector-grade presentation.

Market and Investment Analysis

From a market-structure standpoint, Bonnes-Mares should be approached as a high-prestige, producer-dependent grand cru rather than as a uniformly investable appellation. The broader Burgundy market provides the backdrop. Liv-ex currently shows the Burgundy 150 index at 613.4, up 2.0% over one year, down 9.6% over two years, and up 5.2% over five years. That follows a much more explosive earlier phase: Liv-ex reports that the Burgundy 150 rose 31.0% in 2021, 28.5% in 2022, and had already climbed 168.8% since 2010 by the time of its 2019 classification study. A separate Liv-ex report notes that the same index surged 86.2% between June 2016 and December 2018 before falling 8.8% in 2019. The market interpretation is straightforward: Burgundy has already gone through both runaway appreciation and meaningful correction, and Bonnes-Mares now trades in a more selective environment where brand strength matters more than simple appellation prestige.

At the producer level, the current public data show a very clear hierarchy. iDealwine currently estimates Roumier 2021 at €926, Mugnier 2019 at €903, Dujac 2019 at €639, de Vogüé 2019 at €501, Bruno Clair 2021 at €315, and Arlaud 2019 at €313. Retail snapshots point in the same direction: Roumier 2022 is publicly listed at €1,395, de Vogüé 2022 at €777, Mugnier 2020 at $1,750, and Dujac 2023 around €905 ex-VAT in bond. These are not directly interchangeable data points—some are estimates, some are current offers, and regional taxes differ—but taken together they make one thing plain: the producer premium inside Bonnes-Mares is enormous. That premium is the chief determinant of investment quality, because market depth, critic attention, and resale ease all follow it.

Auction evidence reinforces this conclusion. Christie’s artist and auction pages show Roumier Bonnes-Mares appearing repeatedly in mature and large-format lots, including 2005, 2009, 2012, 2016, and 2018 magnums; Sotheby’s promoted Roumier Bonnes-Mares 2005 in its March 2025 “Legends of Burgundy” sale with a $6,500–8,500 estimate for six bottles; and Acker’s official March 2025 La Paulée release reports three bottles of 1988 Roumier Bonnes-Mares Vieilles Vignes realizing $32,500. Acker further reported in September 2025 that three bottles of 1988 Roumier Bonnes-Mares realized $18,750 each, setting new world records, while a 1961 Vogue Bonnes-Mares brought $6,250. Christie’s-linked coverage in The Drinks Business reported a Domaine Comte Georges de Vogüé Bonnes-Mares 1962 achieving £47,500 in a February 2025 sale. This is not the behavior of an obscure climat with thin demand; it is the behavior of a recognized luxury collectible—but crucially, the records are associated with producer names, pristine provenance, mature vintages, and often rarity of format.

Comparative context is revealing. Official production data show that Bonnes-Mares is almost twice as large as red Musigny and much larger than Clos de Tart, so it is unsurprising that it usually prices below both at the top of the market. Millésima currently lists Comte Georges de Vogüé’s 2022 Bonnes-Mares at €777 per bottle, while the same merchant lists the domaine’s 2022 Musigny Vieilles Vignes at €1,387 per bottle. Clos de Tart 2022 appears around €927 per bottle, while Dujac’s Clos de la Roche 2022 is publicly listed at €899. The analytical reading is that Bonnes-Mares occupies a strong but not absolute summit: it is often more expensive than many neighboring grands crus, yet it does not systematically command Musigny-level money unless the producer itself is already operating in the rarefied trophy category.

My final rating for Bonnes-Mares as an appellation is Selective Buy. For collectors, especially Burgundy specialists, it is close to indispensable because it offers one of the most complete expressions of grand cru Pinot Noir power and longevity. For investors, however, the opportunity is narrower: Roumier, Mugnier, and certain de Vogüé or Dujac vintages can behave like investment-grade assets, but the appellation as a whole is too heterogeneous in liquidity and too dependent on producer branding to qualify as a universal core holding. The strongest strategy is therefore selective concentration, not blanket exposure.

Buyer’s Strategy

For buyers building a serious Bonnes-Mares position, prioritization should be explicit. If the objective is maximum secondary-market strength, Roumier belongs first on the list, followed by Mugnier and de Vogüé, with Dujac close behind for buyers who appreciate its stylistic signature and strong critical backing. If the objective is collector quality with firmer value discipline, Bruno Clair and Arlaud are particularly attractive because their wines remain recognizably grand cru in structure and terroir character while trading at a fraction of the top-end prices. That is not an argument that they will “catch up” to Roumier—there is no hard evidence for that—but rather that they can offer excellent collector utility per euro deployed.

Vintage selection should also be separated by purpose. For long-term cellaring and highest prestige, the best documented targets remain 2005, 2010, 2015, 2019, 2020, and 2022; these years are repeatedly described by BIVB or Jancis Robinson in terms that imply high quality, concentration, and cellaring credibility. For more classical, earlier-drinking Bonnes-Mares, 2021 is explicitly described by both BIVB and Jancis as delicate, lighter, and best approached earlier. For buyers seeking market access without the same scarcity premium, 2023 matters because BIVB describes it as Bourgogne’s largest harvest, which replenished stocks and should make acquisition marginally less strained, even though the best Bonnes-Mares allocations will still remain difficult.

Formats matter. Standard bottles retain the deepest trading pool, but magnums deserve priority when provenance is impeccable and the cellar plan is long-term. Christie’s and Acker both repeatedly feature Bonnes-Mares in magnum or original-case formats, and direct-from-estate or original-case lots are consistently highlighted by the auction houses. In practice, serious buyers should prefer original wooden case, direct domaine or long-established merchant provenance, and complete paper trails where possible. The more expensive the producer, the less wise it is to compromise on these points.

Storage and provenance deserve unusually strict standards here. This is a tannic grand cru often bought for decades rather than years, so the penalties for poor storage are severe. Buyers should look for high fills relative to age, clean capsules, no seepage, labels consistent with period and producer, and where possible original cases or documented ex-domaine history. Too-cheap offers in blue-chip Bonnes-Mares should be treated with suspicion rather than enthusiasm. The existence of Christie’s sales built around numbered labels and personalized back labels from direct estate releases tells you what the top end of the market values most: traceability, condition, and confidence.

The collector’s conclusion is therefore nuanced but clear. Bonnes-Mares is one of Burgundy’s reference grands crus, and for cellar builders who understand producer hierarchy it offers outstanding long-term relevance. Buy the appellation aggressively only when producer, vintage, and provenance all line up. Buy more broadly only if the ambition is connoisseurship rather than resale. In today’s market, that is the right balance between romance and discipline.